You own a house in St. Petersburg and you need it gone. Maybe Helene's surge wrecked the first floor of your Shore Acres rancher. Maybe Citizens non-renewed you and the listing has sat for four months. We pay cash, buy it as-is, and close in 7 days.

Why Sell to Byron in St. Petersburg

- We actually buy storm-damaged homes. Helene's September 2024 surge pushed 4–7 feet of saltwater into Shore Acres, Riviera Bay, Snell Isle, Venetian Isles, and St. Pete Beach. We've cut deals on every one of those streets with mold, drywall, and ruined HVACs still on the curb.

- We close around Citizens non-renewals. A retail buyer needs insurance to get a mortgage. We don't need a mortgage. Your non-renewal letter is not our problem.

- We handle out-of-state heirs. Half of downtown St. Pete's older condo stock is owned by snowbirds whose kids live in Cleveland, Detroit, or Toronto. We sign DocuSign, wire to wherever, and never make you fly down.

- We buy the lot, not the house. If the structure is past 50% damage and FEMA's substantial-improvement rule makes rebuilding the only path, we'll value the dirt and pay for the dirt — you don't have to figure out demo costs.

- We pay your code-enforcement liens at closing. Lealman, unincorporated Pinellas, and St. Pete proper all stack daily fines. Title cleans them up; you don't write a check.

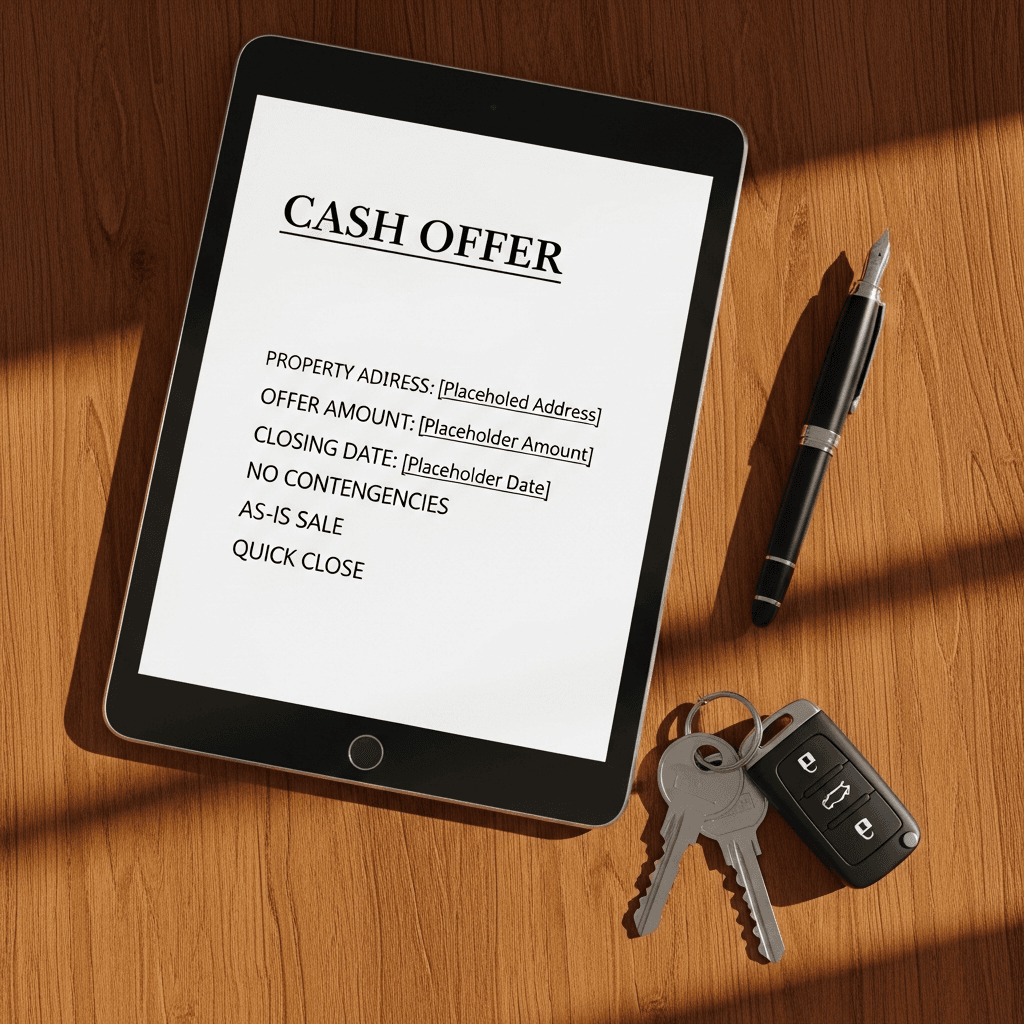

- No commissions, no fees, no inspection-period games. What we offer is what you net.

- One local point of contact. You text Byron. Byron answers. Not a 1-800 call center routing you to a Phoenix wholesaler.

How It Works in St. Petersburg

- Tell us about the house. Address, the rough situation (storm, probate, tired-of-it, divorce), and any liens or insurance claims you know about. Takes about 4 minutes by phone or web form.

- We give you a real cash offer in 24 hours. We pull Pinellas Property Appraiser, FEMA flood-zone maps, post-Helene damage photos, and recent comps for your specific block — not just your zip code. The number we send is the number we close on.

- You pick a closing date at a Pinellas title company. Could be 7 days. Could be 60 if you need time to clear out a snowbird parent's stuff. We work to your calendar, not ours.

Situations We Buy in St. Petersburg

- Hurricane Helene & Milton storm damage — Shore Acres, Riviera Bay, Snell Isle, Venetian Isles, Coquina Key, St. Pete Beach. Flooded, gutted, mold, abandoned mid-remediation — all fine.

- Inherited and probate houses — Old Northeast bungalows, Kenwood craftsmans, Disston Heights ranchers passed from snowbird parents to out-of-state kids.

- Code-enforcement lien properties — overgrown lots, junk cars, unpermitted additions, work-without-permit from a post-Helene contractor who ghosted you.

- Downtown and Old Northeast condos — including units with pending §718.112(2)(g) Milestone/SIRS special assessments.

- Citizens Property Insurance non-renewals — letters dated late 2024 through 2026 are stacking up. We close without a bound policy.

- Insurance-claim-denied homes — Helene claim denied, underpaid, or stuck in §627.70152 pre-suit notice limbo. You don't have to win the claim before selling to us.

- Tear-down lots — Crescent Lake, Old Northeast, Allendale, parts of Lealman where the lot's worth more than the structure post-Helene.

- Pre-foreclosure under Florida's judicial process (Ch. 702) — sell before the §45.031 clerk's sale even if a lis pendens is already recorded.

- Divorce sales under Ch. 61 with a §48.23 lis pendens on title.

- Tax-lien properties with Pinellas tax certificates outstanding under §197.472.

- Tired landlord exits — Lealman, Disston Heights, and South St. Pete duplexes and tenant-occupied SFRs.

St. Petersburg Local Section

St. Pete is not Tampa. Pinellas County is its own market with its own rules, and after Helene that's truer than ever.

Geography that drives our offers. St. Petersburg sits on a peninsula. Tampa Bay to the east, Boca Ciega Bay and the Gulf to the west, two miles of low-elevation neighborhoods sandwiched in between. The Helene surge in September 2024 came in off Tampa Bay, not the Gulf, which is why Shore Acres, Riviera Bay, Venetian Isles, Coquina Key, and the eastern half of Snell Isle flooded harder than St. Pete Beach did. Some of those streets had 4–7 feet of saltwater in the living room. Roughly six months later, FEMA's 50%-substantial-damage rule was forcing teardown decisions on hundreds of homes that got "minor cosmetic damage" stickers on the front door.

Neighborhoods we work in every week:

- Shore Acres — single-story 1950s–60s ranches on slab, near sea level, north of Coffee Pot Bayou. Helene's ground zero. Most listings here now sell either to investors or not at all.

- Riviera Bay — east of 4th Street, Weedon Island side. Same flood story as Shore Acres but a tighter lot grid and more mid-century block construction.

- Snell Isle — older money, tile roofs, larger lots. The eastern edge along Coffee Pot Bayou took surge; the elevated interior didn't. Property-by-property analysis matters here.

- Old Northeast — Granada Terrace through Coffee Pot Park. Bungalows from the 1910s–30s, brick streets, mature live oaks. Sits higher than Shore Acres but the housing stock is 90+ years old, so we see foundation, plumbing, and electrical scope on almost every deal.

- Historic Kenwood — bungalows and craftsmans west of downtown. Designated historic district, which means exterior changes need Community Planning & Preservation Commission review. We know how to price around that.

- Historic Roser Park — small district along Booker Creek, brick-paved switchback streets. Tight inventory, uniqueness premium, but slow-moving for retail buyers because of bridge and slope quirks.

- Crescent Lake — north of downtown around the lake itself. Strong tear-down/rebuild market. R-1 lots with mid-century block houses regularly sell as dirt.

- Disston Heights — north-central, mid-century blockhouses on quarter-acre lots. High concentration of estate sales as the original buyers' kids inherit out of state.

- Lealman — unincorporated, between St. Pete and Pinellas Park. Code enforcement is aggressive; mobile-home and older block-home stock; lots of long-tail tax-lien and lien-stack situations.

- St. Pete Beach — barrier-island, mostly south of the Don CeSar. Mix of 1950s cottages, 70s condos, and short-term rental investment stock. The post-Helene insurance hit on STR cash flow is real and it's pushing owners to sell.

Insurance reality. Citizens Property Insurance non-renewals across Pinellas climbed sharply through 2025 and into 2026 as the carrier worked through depopulation and post-Helene reassessment. A non-renewal letter is not a small problem — under §627.351(6) and the depopulation framework, owners can get pushed to a private offer within 20% of the Citizens premium, and many simply can't underwrite the new number. For owners who were already considering selling, the non-renewal is what tips it. Add a §627.7152 reality check: post-2023 residential policies do not allow assignment-of-benefits, so a homeowner stuck mid-claim can't even sign their check over to a roofer to make the property sellable. Cash sale becomes the path of least resistance.

Snowbird-inherited stock. A meaningful share of downtown St. Pete and Old Northeast condos and small SFRs are owned by retirees who've been here since the 1990s or 2000s. When that owner passes, the heirs are usually in the Midwest or southern Ontario. They don't want to fly down. They don't want to manage a Florida estate. They want a buyer who can sign with the personal representative under §733.607, or close after a §735.201 Order of Summary Administration if the non-exempt estate is under $75,000 (rising to $150,000 under CS/HB 1337 effective July 1, 2026). We close those deals weekly.

Tear-down opportunity. Two things have aligned: Helene's substantial-damage determinations on slab homes, and rising land values in walkable inner neighborhoods (Crescent Lake, Old Northeast outskirts, parts of Allendale). When the math says "demo and rebuild" beats "repair," the existing owner usually doesn't want to be the one to run that play. They don't want to pay an architect, pull a demo permit, sit through the City of St. Pete plan review queue, hire a builder, fight insurance for the structure cost, and then market a brand-new home eighteen months later. They want a buyer who can take it now, in dirt-and-debris condition, and write the check. We do that. We've taken down 1950s slab homes in Shore Acres, run 1920s bungalows past Kenwood's historic-preservation review when worth saving, and platted single tear-downs into permitted infill rebuilds across Disston Heights and Allendale.

Property tax pressure. Pinellas County's millage and the post-Helene reassessment cycle have pushed real-tax bills up across the peninsula. Combined with insurance shocks, owners who were comfortably homesteaded at a $3,500/year tax + $2,800/year insurance combo are now looking at $4,500 + $7,000 — and that's before HOA dues on condos. For a fixed-income retiree in Old Northeast or a snowbird-inheritor in Disston Heights, the carry cost alone is a reason to sell.

The barrier islands. St. Pete Beach, Pass-a-Grille, Treasure Island, and Madeira Beach are technically separate municipalities, but they show up on the same Pinellas closings table we use for St. Pete proper. Helene took out ground-floor units across the barrier islands, and the FEMA 50% rule hit even harder there because lot values are so high — a $400K cottage on a $900K lot can absorb a lot of damage before the determination forces an elevation rebuild. Owners with vacation rentals here have been our most consistent post-Helene call volume.

St. Petersburg-Specific Legal & Practical Hooks

FEMA substantial-damage rule and the 50% trigger. Under the National Flood Insurance Program, a structure in a Special Flood Hazard Area that sustains damage where the cost to repair equals or exceeds 50% of the structure's pre-damage market value must be brought into full current floodplain compliance — typically meaning elevated above base flood elevation. After Helene, the City of St. Petersburg's floodplain management office issued substantial-damage determinations across Shore Acres, Riviera Bay, Venetian Isles, and parts of Snell Isle. Many owners didn't know that even cumulative repairs over time count toward that 50% bucket. If you're sitting on a house where the determination already came back, or you suspect it will, the elevation cost (often $200K+) makes a cash sale to an investor who will tear down and rebuild new construction the cleanest exit. That's the math we underwrite.

Hurricane insurance after the AOB ban. Florida's §627.7152 (residential policies issued on or after January 1, 2023) makes post-loss assignments of benefits void and unenforceable. Translation: you can't hand your Helene insurance check off to a contractor in exchange for a new roof or remediation work — you have to manage the claim, the payout, and the contractor relationship yourself. For homeowners who were counting on AOB to bridge them through repairs, this killed the plan. A cash sale lets you walk away from the open claim entirely; under §627.70152, the pre-suit notice burdens stay with the insured-seller's prior interest, not with the cash buyer who takes the property.

Homestead tax shock for the next buyer (§689.261). Florida law requires a written disclosure that buyers cannot rely on the seller's current property tax bill. When a long-time St. Pete homestead transfers, the property gets reassessed at the purchase price and the Save Our Homes 3% cap (Art. VII §4(d)) drops off. For an Old Northeast bungalow that's been homesteaded since the 1990s, the next year's tax bill can triple. This is why retail listings in Old Northeast, Snell Isle, and Crescent Lake stall — the buyer gets pre-approved on the seller's tax number, then panics when they run the real one. We don't. Our offers price the reassessed bill in from day one. Save Our Homes portability under §193.155(8) lets the seller carry up to $500,000 of accumulated SOH benefit to a new Florida homestead within 3 tax years — worth knowing before you sell, especially if you're rolling proceeds into a smaller, drier inland Pinellas property.

Code-enforcement liens and the Lealman factor. St. Petersburg, unincorporated Pinellas, and Lealman code enforcement run independent dockets, and Helene's aftermath has packed all three with open cases — unpermitted post-storm work, abandoned dryout, blue tarps past 90 days, debris piles, derelict vehicles. Daily fines compound at $250/day on many open code cases, and lien stacks of $20K, $50K, even $100K+ are not unusual on long-tail Lealman addresses. Most retail buyers walk the moment they see the lien report. We don't. We negotiate the liens at the title-company table — many St. Pete code liens settle for cents on the dollar when the new owner commits to bringing the property into compliance, and that work is what we do for a living.

- 15+ years and 500+ Florida closings. This is not our first hurricane.

- BBB A+ accredited and 4.9 stars across 87+ Google reviews.

- Family-owned, direct buyer. No wholesalers in the chain. We sign, we close.

- Pinellas-side closings only. We use Pinellas County title companies because Pinellas docs, Pinellas liens, Pinellas estoppels.

- No "subject to inspection" outs on day 9. When we sign, you can plan around the closing date.

- Cash advance on request. If you need money before closing to clear a contractor lien or move costs, we'll talk.

How fast can you close on a St. Petersburg house?

We close in as little as 7 days at any Pinellas County title company. Most St. Pete sellers pick a date 14–21 days out so they can pack at their own pace. You name the day; we work around it.

Will you buy my Shore Acres or Riviera Bay home if it flooded during Hurricane Helene?

Yes. We bought storm-damaged homes across Shore Acres, Riviera Bay, Snell Isle, and Venetian Isles after the September 2024 surge. You don't have to gut, dry, or remediate anything — leave the drywall on the curb if you want, we'll handle the rest.

Citizens non-renewed my St. Pete house. Can I still sell?

Absolutely. A Citizens non-renewal kills most retail buyers because they can't get a mortgage without insurance. Cash buyers don't need a policy in place to close, so a non-renewal that froze your listing for 6 months can be a closed sale with us in under 2 weeks.

Do you buy inherited St. Petersburg houses still in probate?

Yes — and we can close the same week your Pinellas probate court issues Letters of Administration under §733.607, or an Order of Summary Administration under §735.201 for estates ≤$75,000. We've worked with snowbird heirs in Michigan, Ohio, and Ontario who never want to set foot in Florida.

What about a downtown St. Pete condo with a SIRS special assessment?

We buy condos with pending Milestone or SIRS structural-integrity assessments under §718.112(2)(g). The pending assessment usually shows up in the §718.116(8) estoppel and we price the offer with that number baked in — you walk away clean instead of cutting the association a five-figure check.

Will you buy a tear-down lot in Old Northeast or Crescent Lake?

Yes. St. Pete tear-down lots are some of our favorite buys, especially R-1 and NT-1 zoning west of 4th Street and around Crescent Lake. If FEMA's 50% rule means rebuilding is cheaper than repairing, we already know the math.

I owe more code-enforcement fines than the house is worth. Now what?

St. Petersburg code enforcement can run $250/day on Lealman and unincorporated Pinellas open cases. We negotiate the lien at closing through the title company — sellers regularly walk with money even when the lien stack looked terminal on paper.

Do you buy St. Pete Beach and Treasure Island short-term rental properties?

Yes. Post-Helene STR owners on St. Pete Beach, Pass-a-Grille, and Treasure Island who lost a season of bookings and got hit with assessment shock are a regular call for us. We close cash without the appraisal contingency that's blowing up retail deals on the barrier islands.

How is your offer different from a Tampa Bay wholesaler's?

We're the end buyer. We close on our own balance sheet, in our name, at a Pinellas title company — not a Hillsborough wholesaler trying to assign your contract. If we sign, we close. No "inspection period" bait-and-switch on day 9.

Are there fees, commissions, or closing costs I have to pay?

No commissions. No "admin" or "transaction" fees. We pay the standard seller doc stamps under §201.02 ($0.70 per $100) and the customary Pinellas title costs out of our side. Whatever number we agree on is the number you net at closing.

Ready to Sell Your St. Petersburg House?

Call or text Byron at 951-331-3844. Tell us the address and the rough situation — Helene-flooded Shore Acres rancher, Old Northeast bungalow you inherited from your dad, Snell Isle waterfront with a Citizens non-renewal letter, Lealman duplex with $40K of code fines stacked, downtown condo with a SIRS assessment that just hit. We'll have a real cash number for you within 24 hours, and a Pinellas closing date on your calendar within the week. No pressure. No fees. No fly-down required if you're an out-of-state heir. We've done this 500+ times across Florida — let's do yours next.

If you also own property in Tampa, Clearwater, or Largo, we buy across all of Tampa Bay. One call covers it.