Selling a Fort Lauderdale house — whether it is an aging waterfront home on Las Olas with a soft seawall, an inherited A1A condo facing a six-figure structural assessment, or a Coral Ridge ranch with hurricane damage — does not have to take six months and three contracts. Get a fair cash offer in 24 hours and close in 7 days, as-is.

Why Sell to Byron in Fort Lauderdale

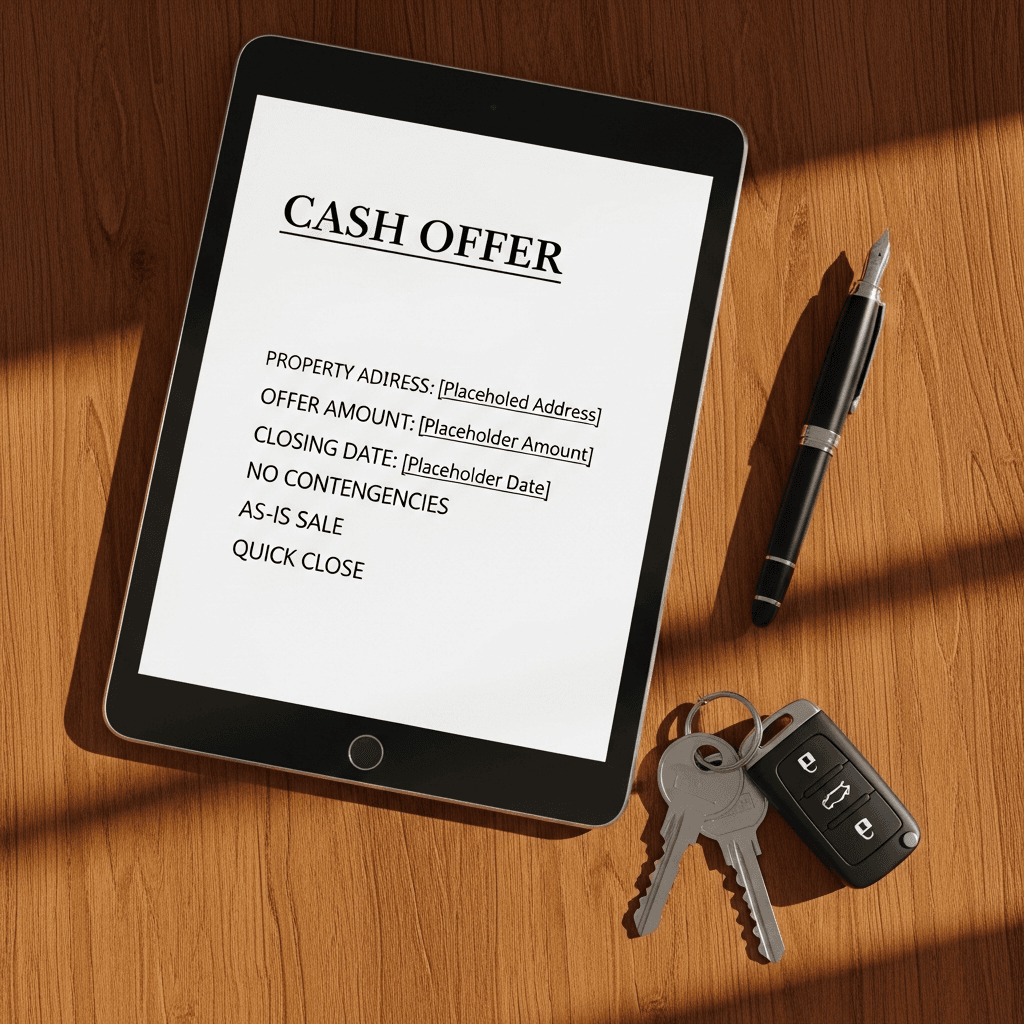

- Cash, not financing. No lender, no appraisal contingency, no buyer dropping out at week six because the underwriter flagged a 1962 roof or an unpermitted addition.

- As-is, every time. Pop-up mold from a slab leak on Tarpon River, a seawall that bowed during Wilma, a kitchen the previous tenant never finished — none of it kills the deal.

- Local Broward closings. We close at Broward County title companies your attorney already knows, on the 17th Judicial Circuit's normal recording cycle.

- 15+ years, 500+ Florida closings, BBB A+. Byron Johnson has been buying Florida houses since 2010, with 87+ Google reviews averaging 4.9 stars. Family-owned, no boiler-room call center.

- We close around your life. Snowbird heirs flying in from Quebec for one weekend, a probate that won't wrap until next month, a divorce judgment that drops in 30 days — we work backward from your date.

- No fees, no commissions, no surprises. The number we offer is the number on the closing statement. Broward custom is for seller to pay owner's title; we cover it.

How It Works in Fort Lauderdale

- Tell us about the property — call 951-331-3844 or fill out the form. Address, condition, situation. Two minutes.

- Walkthrough or virtual review (24 hours) — for waterfront homes we walk the seawall and dock; for condos along A1A and Galt Ocean Mile we usually do photo/video and pull the building's structural report ourselves.

- Written cash offer — same day or next morning. No obligation, no pressure, no follow-up sales calls if you pass.

- Close in 7-14 days at a Broward title company — or whatever date you choose. Funds wired the day of closing.

Situations We Buy in Fort Lauderdale

- Hurricane and flood-damaged homes — roof damage, blown impact windows, finished basements that took on water, soft seawalls

- Inherited houses and condos — especially A1A, Galt Ocean Mile, and Coral Ridge homes left to out-of-state heirs

- Probate properties — both formal administration (§733.607) and summary administration (§735.201)

- Condos with pending Milestone or SIRS assessments — older buildings on the beach or downtown facing post-Surfside special assessments

- Foreclosure properties on the Broward 17th Circuit docket — cash close before the §45.0315 certificate of sale files

- Divorce sales — when a Ch. 61 final judgment requires the marital home to be sold, or one spouse files lis pendens under §48.23

- Tired-landlord rentals — Victoria Park and Flagler Heights duplexes and triplexes with bad tenants and deferred maintenance

- Code-enforcement and open-permit liens — City of Fort Lauderdale Building Department and Community Inspections cases

- Out-of-state owners who never use the property — snowbird condos that haven't seen the owner in three winters

- Vacant homes with rising insurance and association costs you no longer want to carry

Fort Lauderdale Local Section

Fort Lauderdale is the Broward County seat, anchoring a metro of nearly two million people. The city's housing stock breaks into three buckets that drive most of our calls.

Waterfront single-family homes (1950s-1970s). Las Olas Isles, Rio Vista, Coral Ridge, Sunrise Key, Bay Colony, and Harbor Beach are the legacy waterfront neighborhoods — 60 to 75 years old, mostly built with concrete-block construction, almost all on a deepwater canal or the Intracoastal. The challenges that show up over and over: original 1960s seawalls failing (Fort Lauderdale's seawall code requires elevations rising over time), corroded boat-lift footings, hurricane damage from Wilma (2005), Irma (2017), and the king-tide flooding events that have intensified since 2018. Roof age is the silent killer here — a 22-year-old tile roof that has not been recovered will fail any retail buyer's insurance underwriter, and Citizens Property Insurance is no longer writing many of these properties. We buy them as-is.

Pre-war and inland bungalows. Victoria Park, Tarpon River, Sailboat Bend, and Flagler Heights are walkable historic neighborhoods east and west of downtown. The housing stock skews 1920s-1950s wood-frame and Mediterranean Revival, often without modern electrical or plumbing updates, sometimes with locally-designated historic overlays that limit what an investor can do without HARB approval. Estate sales and divorce sales come through these neighborhoods constantly — a long-time owner passes and the kids in another state want a clean exit.

Condos and oceanfront towers. Fort Lauderdale's condo inventory is concentrated on Galt Ocean Mile, A1A from the 17th Street Causeway up to Oakland Park Boulevard, downtown, and the Las Olas corridor. Many of these buildings were built between 1965 and 1985, putting them squarely in the post-Surfside Milestone Inspection cycle (Florida §718.112(2)(g), §553.899). Special assessments for concrete restoration, balcony rebuilds, and structural reserves have ranged from $30,000 on smaller units up to $250,000+ on oceanfront high-rises. Inherited owners — particularly snowbird heirs in New York, New Jersey, Quebec, and Ontario — are choosing to cash out rather than write a check they did not budget for.

We also buy outside the city limits — Wilton Manors, Oakland Park, Lauderdale-by-the-Sea, Lauderdale Lakes, Plantation, Sunrise, Davie, and the rest of Broward — and we close in nearby cities including Hollywood, Pembroke Pines, Pompano Beach, and Miami every month.

Fort Lauderdale-Specific Legal and Practical Hooks

Condo assessments and the Milestone Inspection wave. Under Florida Statute §718.112(2)(g) and §553.899, condominium buildings three stories or higher must complete a Milestone Inspection by their 30th year (25th if within three miles of the coast) and a Structural Integrity Reserve Study (SIRS) every 10 years thereafter. The post-Surfside reforms have hit Fort Lauderdale's older oceanfront stock especially hard. Many associations are passing the cost through as special assessments, and §718.116 makes the buyer take title subject to any unpaid balance. When you sell to Byron, we pull the §718.116(8) estoppel letter ourselves, calculate exactly what is owed, and net it out at closing — no surprise call from the title agent two days before closing telling you to bring $42,000 to the table.

Hurricane damage, AOB reform, and Citizens. For policies issued on or after January 1, 2023, post-loss assignments of benefits are void under §627.7152. That means the contractor who used to take your insurance check, do half a roof, and disappear cannot legally do that anymore — but it also means a lot of owners are stuck negotiating directly with Citizens (§627.351(6)) for months. Public adjusters are capped at 10% of the claim during the first year of a declared emergency under §626.854. The math often pushes Las Olas, Rio Vista, and Coral Ridge owners to sell rather than fight a year-long claim battle on a 1965 home that may need a full reroof anyway. We do not need a clean four-point or wind-mitigation report to close.

Probate, snowbirds, and homestead. Many of the A1A condos and Coral Ridge homes we buy come to us from heirs who never lived in the property. Under §735.201, summary administration is available when the non-exempt estate is $75,000 or less (rising to $150,000 on July 1, 2026 under CS/HB 1337) or when the decedent has been gone more than two years. Formal administration under Ch. 733 is needed for larger or recent estates and the court issues Letters of Administration so the personal representative can sign the deed (§733.607). One trap on homestead property: under Article X §4 of the Florida Constitution, a homestead cannot be devised if the decedent left a surviving spouse or minor child — the property passes by operation of law, regardless of what the will says. We work with your probate attorney and only sign deeds the court can actually enforce.

The Broward closing and the §689.261 tax shock. Broward County is one of the four Florida counties (with Miami-Dade, Sarasota, and Collier) where the seller customarily pays the owner's title insurance premium. Doc stamps on the deed (§201.02) run $0.70 per $100 of price and are also typically a seller cost. Florida's §689.261 disclosure requires the seller to warn the buyer that property taxes will be reassessed at the new sale price, and Save Our Homes protection (Art. VII §4(d)) drops off — for a Coral Ridge owner who has held the home since 1998, the next year's tax bill could be 4-5x what they were paying. Retail buyers regularly back out at this discovery. Cash buyers like us underwrite the new tax basis from the start.

- Real human, not a tech platform. Byron Johnson personally underwrites every Broward offer. Call 951-331-3844 and you are not getting bounced through a call-center queue.

- We pull the title and HOA estoppels ourselves. You do not need to coordinate with an attorney, an HOA manager, or a title company. We do all of it.

- Three offer paths if you want them. Fastest cash close, slightly higher price with 30-45 days, or a creative-finance offer (seller-financed or lease-option) that can clear a much higher price for the right seller.

- We close on properties other investors won't touch. Open permits, code-enforcement liens, expired homestead, mid-probate, mid-divorce, mid-foreclosure — none of it disqualifies a Fort Lauderdale property.

- 15+ years, 500+ closings, 87+ Google reviews at 4.9★. BBB A+ accredited, family-owned, no out-of-state private-equity rollup.

See the FAQ block at the top of the page for full answers covering:

- How fast we can close on a Fort Lauderdale house

- Whether we buy hurricane and flood-damaged waterfront homes

- Pending Milestone Inspection and SIRS condo assessments

- Inherited A1A condos and pre-probate contracts

- Open permits and City of Fort Lauderdale code violations

- Fees, commissions, and Broward closing costs

- Back HOA and condo association dues

- Buyer homestead-tax shock and how it affects your offer

- Selling during an active Broward foreclosure

- Which Fort Lauderdale neighborhoods we buy in

Ready to Sell Your Fort Lauderdale House?

Whether you are staring at a Milestone Inspection notice, a §45.0315 foreclosure sale date, a Broward probate that won't end, or just a Las Olas waterfront house you no longer want to maintain — call Byron at 951-331-3844 or send your address through the form. You will have a written cash offer in 24 hours, you will know exactly what you walk away with, and you will pick the closing date. No fees, no commissions, no obligation, no pressure.