Miami doesn't sell houses the way the rest of Florida does. The probate calendar is the longest in the state, the condo law moves under your feet every year, and your buyer either speaks Spanish or loses the deal. Byron pays cash, closes in 7 days, and meets you where you are.

Why Sell to Byron in Miami

- Local Miami-Dade closings. We close at title companies on Brickell Avenue, in Coral Gables, in Doral, and in Kendall — wherever is closest to you. No flying anyone in.

- Hablamos español. Cuban, Venezuelan, Colombian, Puerto Rican, Dominican — we work the deal in the language your family makes decisions in.

- We take the violations. Open Code Enforcement file in Allapattah? Unpermitted addition in Little Havana? Daily $250 fines on a Liberty City rental? We absorb all of it post-closing.

- We know the condo law. Florida Statute 718 changes every legislative session. We track Milestone Inspections, SIRS reserves, ROFR clauses, and the estoppel process. We will not get caught at the closing table.

- Cash buys don't need a lender. No appraisal, no lender disclosure window, no buyer financing contingency. The only timeline is title.

- 15 years, 500+ FL transactions, BBB A+. Family-owned. Byron answers his own phone at 951-331-3844.

- No fees, no commissions, no repairs. You get the offer in writing within 24 hours and you keep every dollar of it.

How It Works in Miami

Step 1 — Tell us about the house. Call or text Byron at 951-331-3844, or fill out the form. We need the address, your situation, and the rough condition. If it's a condo, we ask which building so we can pull the most recent Milestone status.

Step 2 — Walkthrough or virtual review. We meet you at the house — same week in most cases. For out-of-state heirs (very common in Miami), we do this by video. We pull comps from the actual block, not the MLS average for the zip.

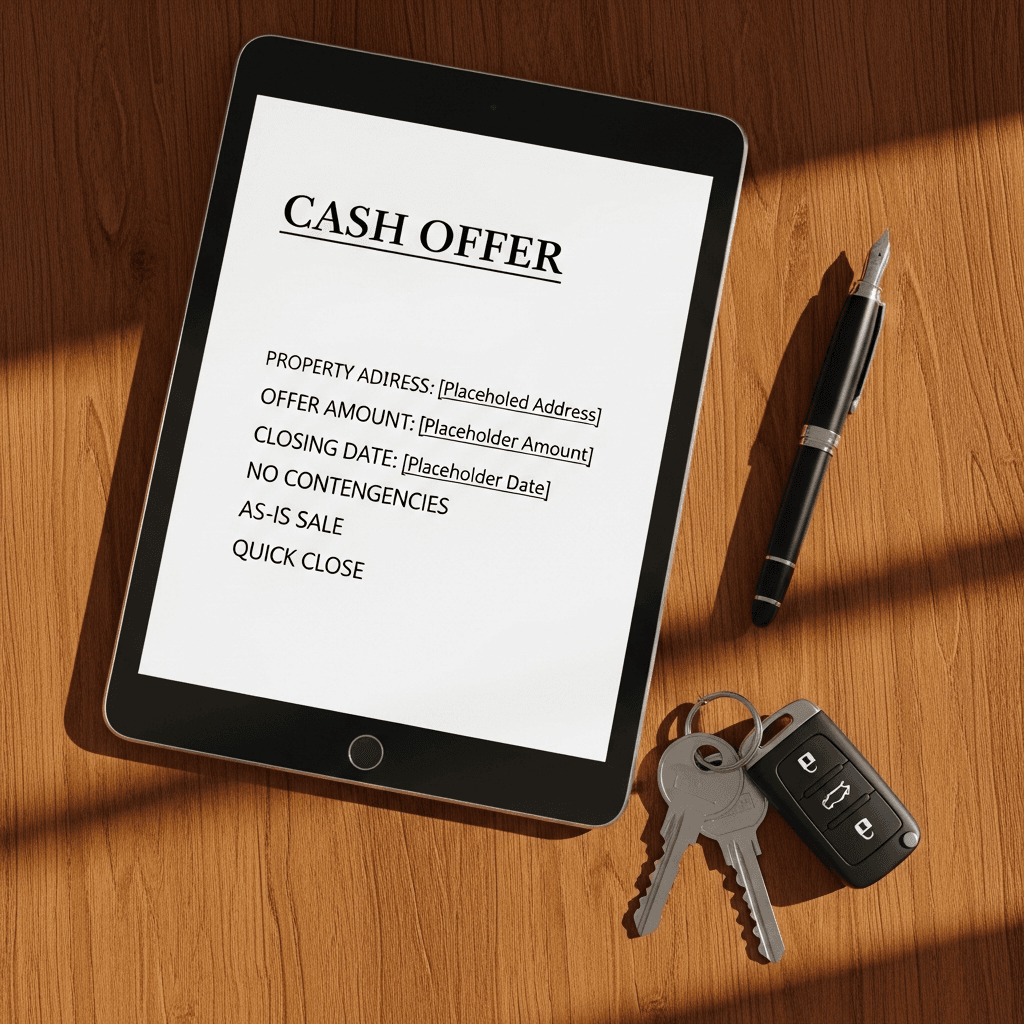

Step 3 — Written cash offer in 24 hours. No-obligation. The offer is on the FAR/BAR "AS IS" Residential Contract (ASIS-7), the same form Florida Realtors and the Florida Bar publish. You read it with your attorney if you want.

Step 4 — Close at a Miami-Dade title company. As fast as 7 days, or the date you pick. Miami-Dade is one of the four Florida counties where the seller customarily pays for owner's title insurance — we pay it. Doc stamps run $0.60 per $100 plus surtax. We cut you a wire or a cashier's check.

Situations We Buy in Miami

- Inherited houses across Miami-Dade. Mom's place in Westchester. Abuela's house in Little Havana. The duplex on NW 22nd in Allapattah. Sell a Miami inherited house.

- Probate properties — Miami-Dade has the highest probate volume in Florida. Whether you're in Summary Administration under §735.201 or Formal Administration with a Personal Representative under §733.607, we'll close on the Miami probate property once you have authority to sign.

- Hurricane-damaged homes. Andrew (1992), Wilma (2005), Irma (2017), and the storm seasons since have left a trail of un-rebuilt roofs, water-damaged drywall, and tarped patios across the county. We buy hurricane-damaged Miami homes.

- Pre-foreclosure and foreclosure-auction homes. Florida is a judicial foreclosure state. Once the lis pendens hits the Miami-Dade Clerk under §48.23, you have 6–14 months — and you can stop the Miami foreclosure by selling for cash any time before the certificate of sale.

- Code-violation properties. Open files at the City of Miami Code Enforcement, City of Miami Beach Code Compliance, or Miami-Dade County Code — daily fines, recorded liens, even foreclosure-by-municipality. We buy Miami homes with code violations.

- Condos with HOA assessments and Milestone deficiencies. Brickell, Coconut Grove, Coral Gables, Aventura, Sunny Isles. Sell your Miami condo fast.

- Single-family houses, any neighborhood. Concrete-block-and-stucco ranches, Mediterranean revivals, mid-century modern, Spanish colonial. Sell a Miami single-family house.

- Tired-landlord rentals with bad tenants in place. Yes — we close with the tenant in occupancy. Section 8, holdover, full lease, doesn't matter.

- Out-of-state and out-of-country heirs. Canada, New York, New Jersey, Venezuela, Colombia, Cuba. We close by Remote Online Notarization.

- Divorce-driven sales. Equitable distribution under Ch. 61, lis pendens during dissolution under §48.23, and exclusive-use orders under §61.077 — we work with both spouses' attorneys.

Miami Local Section

Miami is not a single market. It's a stack of submarkets that price, transact, and litigate completely differently.

Brickell (33129, 33131) is condo land — the densest high-rise corridor in the southeastern United States. The 1980s and 1990s towers along Brickell Bay Drive are the buildings most affected by the post-Surfside Milestone Inspection wave. We've closed on units where the special assessment came in at $80,000 per door three weeks before closing, and we still funded.

Coral Gables (33134, 33146) is single-family money — Mediterranean revivals from the 1920s, oak-canopy streets, deed restrictions enforced by the Coral Gables Historic Preservation Board. Half the houses we look at here have unpermitted additions from the 1960s through 1990s, because the Gables permit office is famously tight. We don't care — we close anyway.

Little Havana (33125, 33135) is the heartland of multi-generational Cuban families. The houses on SW 8th Street and the side streets off Calle Ocho are concrete-block-and-stucco from the 1940s and 1950s. Many have been in the same family for 50 years. When abuelo passes, the estate is typically split four to seven ways across heirs in Miami, Tampa, New Jersey, and Hialeah. We do the probate math, we make one offer, and the family doesn't have to argue about it.

Wynwood (33127) has been re-zoned twice in the last decade. The Wynwood NRD-1 overlay changed the highest-and-best-use of nearly every parcel south of NW 36th Street. Many of the small wood-frame and CBS houses still in the district carry development-rights value the owner doesn't realize. We pay for that, not for the dilapidated structure.

Allapattah (33125, 33142) is the next neighborhood in the gentrification wave. The 1940s–1960s housing stock is rough — we see active code-enforcement files in roughly 30% of the houses we visit here. City of Miami Code Compliance fines accrue at $250 per day per violation; we've seen liens north of $90,000 on a $300,000 lot.

Liberty City (33147, 33150) carries some of the oldest concrete-block stock in the city. Many homes were built under the post-WWII Liberty Square plan and the surrounding HUD-financed expansions. Title chains here often carry two or three open mortgages, decades-old recorded liens, and disputed heir claims. Slow title — but we work through it.

Kendall (33156, 33176, 33186) is the suburban heart of Miami-Dade — single-family ranches, '70s and '80s subdivisions, and 1990s gated communities. Hurricane Andrew leveled portions of South Kendall in 1992, and you can still see the patchwork rebuild quality in the construction details. Many houses got new roofs only after Wilma in 2005, which means roof age is now 20+ years — and roofs over 15 years are why Citizens is non-renewing policies across the county.

Coconut Grove (33133) is sailboat money on the bay side, and 1920s wood-frame cottages on the inland side. The Grove also carries a steep flood profile — most of the bayfront and Tigertail Avenue corridor sits in VE or AE zones. We don't require a buyer to qualify for flood insurance; we close cash and self-bear the risk.

Pinecrest (33156) is high-equity, high-acreage, and almost entirely homestead. The houses are 1950s–1990s ranches and contemporary builds on half-acre to acre lots. The biggest seller-side issue here is Save Our Homes shock — owners who've held since the '90s have an assessed value 75% below market value, and the buyer's tax bill the next year is unrecognizable.

Westchester (33144, 33165) is solidly Cuban-American single-family, mostly 1960s CBS ranches. Multi-generational ownership, lots of in-law suites, lots of unpermitted enclosed-Florida-room additions from the 1980s. We buy them as-is. Many Westchester houses we look at are owned by the second generation now — adult children whose parents bought the place new in 1965 for $18,000 and held it through Andrew. The market value is north of $600,000. The mortgage is paid off. The kids live in Plantation or Tampa or Atlanta. Nobody wants to manage a vacant house from out of town. That's our typical Westchester deal.

Doral (33122, 33166, 33178) is the Venezuelan capital of the United States — locals call it "Doralzuela." 1990s and 2000s subdivisions, mostly two-story stucco-and-tile. The submarket has been hammered by the post-2014 Venezuela diaspora cycle: families bought during the Maduro exodus, lost income when sanctions hit cross-border money transfers, and now need to liquidate fast to fund moves to Madrid or Bogotá. We close in Spanish, by RON, with international wires.

Hialeah-adjacent corridors (33012, 33013, 33016) — while Hialeah is its own city with its own Byron landing page, the unincorporated Miami-Dade pockets that border it (parts of West Hialeah, Westchester East, and Country Club) follow the same playbook: dense, working-class, predominantly Cuban first- and second-generation owners. We work the entire belt the same way.

The probate volume. Miami-Dade County's Eleventh Judicial Circuit Probate Division processes the highest probate caseload of any Florida county — by a wide margin. The court sits at 73 W. Flagler Street downtown. If the estate qualifies for Summary Administration under §735.201 (currently estates ≤ $75,000, rising to $150,000 effective July 1, 2026 under CS/HB 1337), the order can issue in weeks. Formal Administration under Ch. 733 takes longer, but Letters of Administration generally get to the Personal Representative within 60–90 days of filing. We've signed contracts pre-Letters and closed the day Letters issued.

The Hurricane Andrew legacy. August 24, 1992. Andrew destroyed or severely damaged 125,000+ Miami-Dade homes. The rebuild that followed produced two distinct cohorts of housing stock: pre-Andrew (built to the old South Florida Building Code) and post-Andrew (built to the dramatically tougher 1994 SFBC and then the 2002 Florida Building Code). When you sell a pre-Andrew home today, your buyer's insurance carrier scrutinizes wind mitigation, roof straps, and shutters far more than they would on a post-Andrew build. That's why so many pre-Andrew owners hit the cash-buyer market — the retail buyer can't get a Citizens or admitted-carrier policy on the house without expensive remediation.

Post-Surfside condo realities. The June 24, 2021 collapse of Champlain Towers South in Surfside changed every Florida condo transaction. Senate Bill 4-D (2022) and the 2023/2024 follow-on bills wrote two new requirements into Chapter 718: Milestone Inspections under §553.899 (Phase 1 at year 25 or 30 depending on coastal proximity, Phase 2 if substantial structural deterioration is found) and Structural Integrity Reserve Studies (SIRS) under §718.112(2)(g). Associations that hadn't funded reserves for decades are now passing six- and seven-figure special assessments. Owners who can't afford the assessment are dumping units. We buy those units.

Miami-Specific Legal & Practical Hooks

The condo association problem. Florida Statute §718.112(2)(i) lets a condominium declaration grant the association a right of first refusal or an approval right over unit transfers. Many older Brickell, Coconut Grove, and Aventura buildings have ROFR language baked in from the 1970s and '80s. The board has a defined window (typically 30 days) to either approve the buyer, exercise the ROFR, or step aside. On top of that, §718.116 makes the unit jointly and severally liable for unpaid assessments — a buyer takes title subject to the prior owner's delinquencies. You and your closing agent must request an estoppel letter under §718.116(8) to confirm the exact dollar figure due. We've seen estoppels come back $3,000 and we've seen them come back $147,000. Either way, we factor it in and close.

The post-Surfside reality. Under §553.899 and §718.112(2)(g), buildings three habitable stories or taller and 25–30 years old must complete a Milestone Inspection. If the engineer finds substantial structural deterioration, the building moves to a Phase 2 inspection and the association must fund repairs. SIRS requires the association to commission a reserve study every ten years and fund the reserves on the schedule it specifies. The result: associations that had been waiving reserves for years are now passing eye-watering special assessments. Florida law also addresses condominium termination at §718.117, which is why some buildings — particularly older ones in Bal Harbour, Surfside, North Bay Village, and along Brickell Bay Drive — are exploring termination and bulk sale to developers. We buy individual units in any of those scenarios.

Code Enforcement in Miami. The City of Miami Code Compliance Department, Miami-Dade County Code Enforcement, and the City of Miami Beach Code Compliance Division each operate Special Magistrate hearings under Chapter 162, Florida Statutes. Daily fines typically run $250 per violation, accruing until the property is brought into compliance. Recorded liens become foreclosable. Allapattah, Little Havana, Liberty City, and parts of Westchester carry the heaviest active-violation rates in the county — partly because the housing stock is older, partly because absentee ownership is common. We pay cash, take title with the violations attached, and run the lien-reduction hearing process ourselves after closing.

Homestead and the Save Our Homes shock. The Florida constitutional homestead at Article X §4 protects forced sale and limits devise — if you have a surviving spouse or minor child, the homestead cannot be devised except to the spouse (when no minor child). The tax homestead at §196.031 ($51,411 base exemption for 2026) and the Save Our Homes 3% assessment cap (Article VII §4(d)) are why so many long-tenured Miami families have tax bills 70–80% below market. Florida Statute §689.261 requires us to disclose to the buyer that taxes will reassess at purchase price — but if you're the seller, your final bill is just prorated to closing day. If you're moving to another Florida home, you may port up to $500,000 of accumulated SOH benefit under §193.155(8) within three tax years.

Miami-Dade closing custom. In Miami-Dade County (along with Broward, Sarasota, and Collier), the seller customarily pays for the owner's title insurance policy. Title premium rates are promulgated by the Florida Department of Financial Services under §§627.7711–627.7865 — they are not negotiable. Doc stamps on the deed run $0.60 per $100 of consideration in Miami-Dade plus the discretionary surtax under §201.02, customarily a seller expense. We pay all of these out of the gross offer; there are no closing costs to you beyond what's stated.

Insurance non-renewal and the uninsurable Miami house. Citizens Property Insurance Corporation, the state-run insurer of last resort under §627.351(6), has been dropping Miami-Dade policies at unprecedented pace — particularly on roofs over 15 years old, on pre-2002 wind-mitigation profiles, and in coastal AE/VE zones. The 2022 AOB reform at §627.7152 and §627.7153 made post-loss assignments of benefits void on residential policies issued after January 1, 2023, which means a roofer can no longer take an insurance check from the homeowner. The result: Miami homeowners with old roofs and open hurricane claims are stuck. They can't sell to a financed buyer (no insurance, no mortgage). They can sell to us. We buy uninsurable Miami houses every month — pre-Andrew CBS ranches in Kendall, 1970s wood-frame in The Roads, 1950s bungalows in Coconut Grove. Cash doesn't need a policy to fund.

Lis pendens and the foreclosure clock. Florida is a judicial foreclosure state under Chapter 702. The Miami-Dade Clerk records the lis pendens under §48.23 the moment the bank's complaint is filed at the Eleventh Judicial Circuit at 73 W. Flagler. From that day, the homeowner typically has 6–14 months before the clerk's sale — but the right of redemption ends at the filing of the certificate of sale under §45.0315. Practically, that means we can buy your house any day before the clerk files the certificate. We've closed at 4:00pm the day before a 9:00am Miami-Dade auction.

- You talk to Byron, not a call center. 951-331-3844. Byron answers. 15 years in real estate, 500+ Florida closings.

- Family-owned, not a hedge fund. We're not Opendoor. We're not Offerpad. We're not a national franchise farming a sub-licensee in your zip. We are one family that has been doing this since 2010.

- BBB A+, 4.9 stars, 87+ Google reviews. Local reputation we can't afford to burn.

- We close — actually close. Most "cash" offers re-trade at inspection or at appraisal. We don't get appraisals. We don't re-trade. The number on the contract is the number that wires.

- Bilingual operations. English, Spanish, and the cultural fluency to negotiate with a Cuban abuela the same way you'd negotiate with a Brickell condo board. Both matter.

- We take the messy ones. Open probate. Five heirs. Code violations. Open Citizens claim. Tenant in possession. Special assessment due Friday. We've seen it. We close.

- We work the regional corridor too. If your situation spans multiple cities — say a Miami house and a Tampa property, or a Miami condo with a Fort Lauderdale backup unit — we can write one offer covering both. Most cash buyers won't.

- Documented track record. Every closing we've done in Miami-Dade is filed at the Clerk of Court — public record. Ask us for addresses and we'll send a list.

(See FAQ block in frontmatter — rendered with FAQPage schema.)

Ready to Sell Your Miami House?

Pick up the phone. Byron's number is 951-331-3844 and he answers it himself. Tell us where the house is — Brickell, Coral Gables, Little Havana, Westchester, Pinecrest, Liberty City, anywhere in Miami-Dade — and what the situation is. We'll have a written, no-obligation cash offer in your inbox within 24 hours. If it works, we close in 7 days at a Miami-Dade title company. If it doesn't, you've lost nothing but the phone call. No fees. No commissions. No repairs. No pressure. Hablamos español. Llámenos hoy.