You don't need to fix the roof. You don't need to settle with Citizens first. You don't even need to fly down from Cleveland or Toronto to sign. We buy Cape Coral houses as-is, with open Ian claims, in any flood zone, and we close in seven days at a Lee County title company you choose.

Why Sell to Byron in Cape Coral

- We buy with open Hurricane Ian claims still in mediation. No need to wait out Citizens. We close, you keep the claim path your attorney recommends.

- We buy in flood zone X, AE, and VE. No lender means no flood-insurance hurdle.

- We buy vacant lots — single, double, gulf-access, dry inland. Cape Coral has 100,000+ vacant lots. We've bought from owners in 38 states and four countries.

- We close cash in 7–14 days at any Lee County title company. No appraisal contingency. No financing fall-through.

- No fees, no commissions, no repair list. You take what you want, leave what you don't, walk with a wire.

- We work remotely. Florida allows remote online notarization. You sign from your couch. We wire your proceeds the day the deed records.

- 15+ years, 500+ Florida closings, BBB A+, 4.9★ across 87+ Google reviews. Family-owned. We answer the phone — Byron's cell is 951-331-3844.

How It Works in Cape Coral

- Tell us about the house. Address, condition, what Ian did or didn't do to it. Five-minute call or the form on this page.

- We pull the file ourselves. Lee County property card, FEMA flood determination, code-enforcement search, lien search, plus a desktop comp from recent SW/NW/NE/SE Cape sales. You don't have to lift a finger.

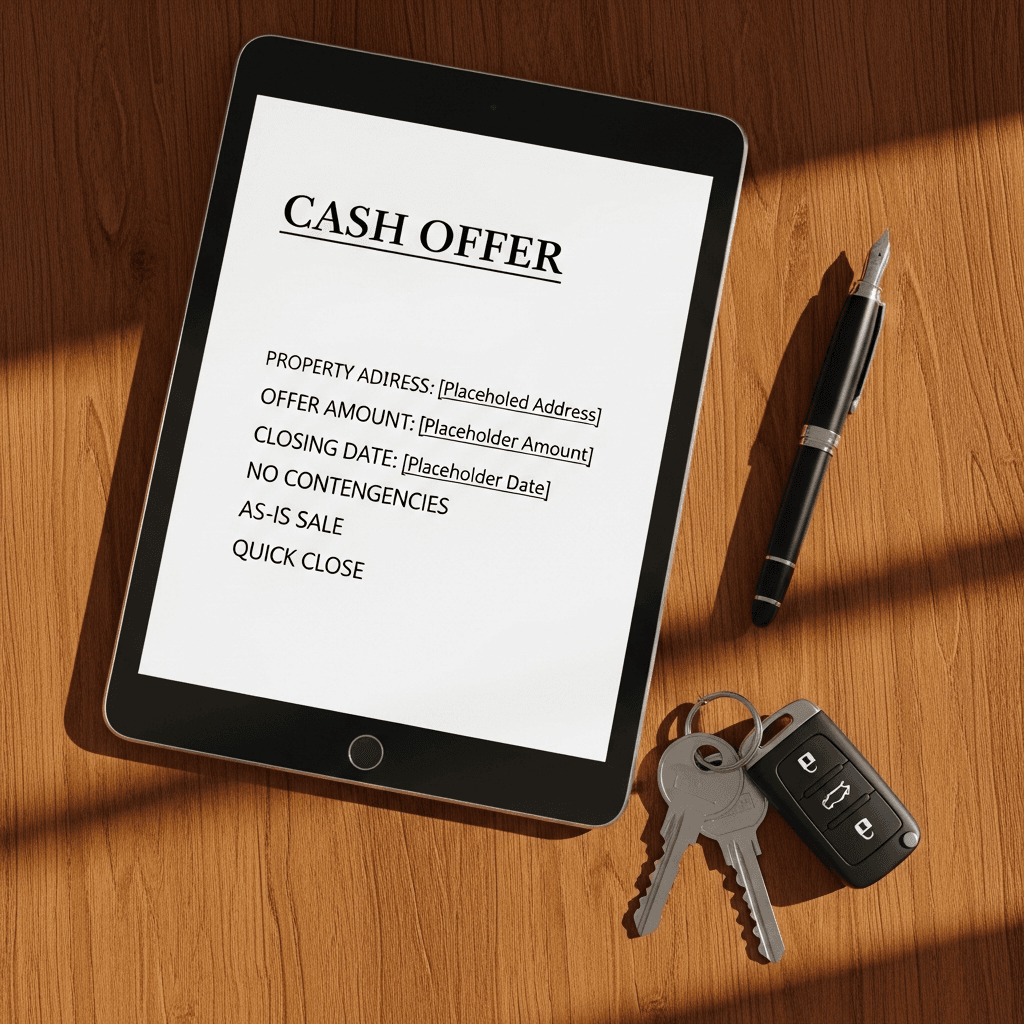

- You get a written cash offer in 24 hours. Real number, real proof of funds, real Lee County title company on the contract — usually Stewart, Old Republic, or a local boutique like Sunbelt Title. You pick the date.

- We close at a Lee County title company. Seven to fourteen days normal; five days when it has to happen. RON if you're out of state. Wire hits the same day the deed records.

Situations We Buy in Cape Coral

- Hurricane-damaged homes — Ian, Helene, Milton, future storms. Roof damage, slab settlement, seawall collapse, lanai destruction, mold from saturated drywall.

- Open Citizens or private-carrier claims. We buy with the claim still alive.

- Citizens non-renewal letters. When the next quote is $11,000 a year and you can't make the math work.

- Inherited houses — formal or summary administration. Out-of-state heirs welcome. We've closed dozens of Cape Coral probates with PRs in Ohio, Michigan, and Ontario.

- Snowbird burnout. Canadian and Northern owners dumping the second home after one too many storms, one too many insurance hikes, one too many condo assessments.

- Vacant lots. Single lots, double lots, triple lots, gulf-access canal lots, freshwater-canal lots, dry inland lots in NW and NE Cape.

- Single-family houses needing rehab. 1970s and 1980s SW Cape ranches with old electrical, polybutylene plumbing, and original roofs.

- HOA-assessed properties in Sandoval, Tarpon Point, Cape Harbour, and other gated communities.

- Code-enforcement liens from the city of Cape Coral — overgrown lot violations, unpermitted lanai enclosures, sea-wall non-compliance.

- Tired-landlord situations — long-term tenants, vacation rentals, post-Ian rent rolls that fell apart.

- Pre-foreclosure with a Lee County circuit court case filed and a lis pendens recorded.

- Lehigh Acres adjacent — including Chinese drywall homes from the 2006–2009 build-year cohort.

Cape Coral Local Section

Cape Coral is its own animal. The city sprawls across 120 square miles of pre-platted Gulf American Land Corporation lots from the late 1950s and 1960s — the largest planned community in Florida history. The result: more than 400 miles of canals (more than Venice, Italy), the largest residential canal system on Earth, and somewhere north of 100,000 vacant residential lots that were sold sight-unseen to Northerners decades ago and never built on.

That history shapes everything about selling a Cape Coral house. The owner of record on a vacant lot in NW Cape might live in Buffalo and have inherited the lot from a grandfather who bought it in 1962 for $895 down. The Ian-damaged ranch in SW Cape might be owned by a snowbird couple in Toronto who flew down twice a year and now can't afford the insurance, the special assessment, and the repairs. We see both stories every week.

The neighborhoods we buy in:

- SW Cape Coral — the most established quadrant. Older 1970s and 1980s ranches, gulf-access canals on Bimini Basin and Yellow Fever Creek, the Cape Coral Yacht Club, Tarpon Point, Cape Harbour, Rotary Park. Took heavy storm surge from Ian; many homes still in repair limbo.

- NW Cape Coral — newer construction, Burnt Store Road corridor, freshwater canals, large vacant-lot inventory. Less Ian damage but more inland flooding from saturated soils.

- NE Cape Coral — north of Pine Island Road, mix of vacant lots and 2000s-era builds. Coral Oaks Golf Course area. Insurance non-renewals running heavy here.

- SE Cape Coral — bordering Fort Myers, Cape Coral Parkway corridor, older inventory and the city's commercial spine. Easier comps, more transactions.

- Pelican — the gated golf-course community in the SW. Custom homes, canal lots, HOA assessments tied to clubhouse and golf-course rebuilds post-Ian.

- Tarpon Point — high-end SW, gulf-access, the Westin Cape Coral, marina condos. Ian damage was significant; assessments are still working through.

- Cape Harbour — gated SW community at the end of Cape Coral Parkway. Mix of single-family and condos. Active assessment work post-Ian.

- Sandoval — Pine Island Road gated community, lakefront homes, HOA-managed amenities. Less direct Ian damage but plenty of insurance pressure.

- Trafalgar — a north-of-Cape-Coral-Parkway pocket with classic SW Cape ranches. Heavy Ian-storm-surge zone. Lots of repair-limbo houses still on the market.

Neighboring areas we also cover (ask about a multi-property deal): Fort Myers, Lehigh Acres, Punta Gorda, Port Charlotte, and down the coast to Naples.

Cape Coral-Specific Legal & Practical Hooks

Hurricane Ian and the AOB shutdown. When Hurricane Ian made landfall on Sept. 28, 2022, just south of Cape Coral as a Category 4 with 150-mph winds, the storm surge — 10 to 15 feet in some pockets of SW Cape and Fort Myers Beach — destroyed thousands of homes and damaged tens of thousands more. Three years later, the rebuild is still grinding. Part of the slowdown is policy: Florida's 2023 reforms (§627.7152 and §627.7153) effectively voided post-loss assignments of benefits on residential policies issued after Jan. 1, 2023, which removed the contractor-driven AOB pipeline that used to fund roof and water-damage repairs upfront. For homeowners with claims that opened in 2022 — Ian — pre-reform AOB rules still apply, but compliance is strict and many claims have been kicked into mediation or pre-suit notice under §627.70152. The practical effect for Cape Coral sellers: if you're 30+ months into a Citizens or private-carrier dispute and you just want out, you don't have to settle the claim before you sell. We close on the house and we structure the claim assignment in a way that works for your insurance attorney.

Citizens Property Insurance and the non-renewal wave. Citizens Property Insurance (§627.351(6)) is Florida's last-resort insurer, and Cape Coral has one of the highest Citizens-policyholder concentrations in the state. The depopulation rules require Citizens policyholders to accept private-carrier offers within 20% of the Citizens premium — meaning if a private carrier quotes you $9,000 against a Citizens premium of $7,500, you have to take the private offer or lose Citizens coverage. Combine that with 4-point inspection failures on 1970s/80s SW Cape ranches (Federal Pacific panels, polybutylene plumbing, 20+-year-old roofs) and wind-mit downgrades after Ian, and the result is a steady drip of Cape Coral homeowners getting non-renewal letters and discovering they can't replace the coverage at any reasonable price. We've closed dozens of those deals. We don't need insurance to fund.

Vacant land, ERPs, and the SFWMD line. Cape Coral sits inside the South Florida Water Management District (SFWMD) jurisdiction. Many of the older platted lots in NW and NE Cape were drawn before modern wetland-delineation rules, and a percentage of them carry ERP issues under Ch. 373 Part IV F.S. and F.A.C. 62-330 — meaning the lot looks buildable on a satellite image but a formal §373.421 wetland delineation reveals jurisdictional waters that wipe out half the buildable footprint. Add the Coastal Construction Control Line (§161.053) for lots near the gulf, and the city of Cape Coral's own utility-extension fees (water/sewer assessments running $20K–$30K+ on lots that aren't on city utilities), and you have a vacant-lot market that scares retail buyers off. We buy these. We pull the wetlands determination, the SFWMD jurisdiction file, and the city's utility status ourselves before we make the offer, and we close.

Homestead, snowbirds, and the §689.261 disclosure. A lot of Cape Coral sellers are out-of-state owners who never claimed Florida homestead — second home, vacation rental, snowbird condo. That actually simplifies the sale: there's no Save Our Homes assessment cap dropping off and shocking the next owner's tax bill, and the §689.261 disclosure (which warns the buyer that the prior owner's tax basis won't carry over) is straightforward. For those Cape Coral owners who did homestead and are now relocating elsewhere in Florida, the §193.155(8) portability provision lets you carry up to $500,000 of accumulated SOH benefit to the next FL homestead within three tax years — worth knowing before you sell.

- We've actually closed in Cape Coral with open Ian claims. Not theoretically. With Citizens, with Heritage, with Citizens-takeout carriers. Talk to our title coordinator — she'll walk you through three recent closings.

- We buy vacant lots most investors won't touch — wetlands-impacted, no city utilities, owner-of-record in another country, decades of unpaid HOA dues from a phantom 1960s POA.

- We pull the file ourselves. You don't fax us anything. We pull the property card from the Lee County Property Appraiser, the FEMA flood determination, the recorded docs from the Lee County Clerk, and the code-enforcement history from the city. Saves you a week.

- Local title companies, real proof of funds, real Lee County addresses on the closing docs. We don't drag deals to a P.O. box in Delaware.

- Family-owned, BBB A+, 4.9★. Byron answers his cell at 951-331-3844. If something goes sideways, you talk to the owner, not a call-center rep.

(See full FAQ schema rendered above and inline below.)

Will you buy my Cape Coral house with an open Hurricane Ian insurance claim?

Yes. We close on Cape Coral homes with open Citizens or private-carrier claims every month. Florida's 2023 AOB ban (§627.7152) means you can't sign your claim over to a contractor anymore, but you can absolutely sell the house and keep your right to pursue the claim. We'll structure the contract so you assign the claim, retain it, or settle and split — whichever path your insurance attorney recommends.

Do you buy in Cape Coral flood zone X, AE, or VE?

All of them. Most of Cape Coral is mapped X, AE, or VE under the FEMA 2021 Lee County maps. We don't need flood insurance to close because we close cash — there's no lender requiring it. AE and VE properties trade at a discount because rebuild costs and elevation requirements are higher under FEMA's 50% substantial-improvement rule, but we still buy them.

Will you buy a Cape Coral home with foundation damage from Hurricane Ian?

Yes. Ian's storm surge and saturated soil caused settlement, slab cracking, and seawall failure across SW Cape, Pelican, and the canal-front pockets of NE Cape. Foundation damage scares retail buyers and kills financed deals, but we pay cash and budget the repair into our offer. Send photos or an engineer's report if you have one — we close as-is on the FAR/BAR As-Is contract.

Can you close on a Cape Coral house if Citizens just non-renewed me?

Yes — non-renewal is one of the most common reasons Cape Coral owners call us. The roof age, 4-point inspection failure, or wind-mit downgrade that triggered Citizens' non-renewal won't stop a cash sale. We don't need insurance to close.

Do you buy vacant lots in Cape Coral?

Yes. Cape Coral has more than 100,000 vacant residential lots — more than any other city in Florida — and we buy single lots, gulf-access canal lots, freshwater-canal lots, and dry inland lots. We pull the wetlands determination, the SFWMD jurisdiction, and the city's utility-extension status ourselves.

I'm an out-of-state owner. Can I sell my Cape Coral house remotely?

Yes — we close roughly half our Cape Coral deals with sellers in Ohio, Michigan, New York, New Jersey, Illinois, and Ontario. Florida allows remote online notarization (RON) under §117.201, so you can sign the deed and closing package from your living room.

Will you buy a Lehigh Acres or Cape Coral home with Chinese drywall?

Yes. Cape Coral and Lehigh Acres took the brunt of the 2006–2009 Chinese drywall (KPT-marked) imports. Most retail buyers and every lender will refuse a known-CD home. We close cash and remediate post-closing.

How fast can you close on a Cape Coral house?

Seven to fourteen days at any Lee County title company. The only delay is pulling the title commitment, the estoppel (if there's an HOA), and the municipal lien search. If you're up against a foreclosure sale, a probate deadline, or a pending Citizens lapse, tell us — we've closed in five days when it had to happen.

Do you buy Cape Coral houses still under HOA assessment for hurricane repairs?

Yes. Some Cape Coral communities — Sandoval, Tarpon Point, Cape Harbour — pass special assessments for canal-wall repairs, roof replacement, or pool deck rebuilds. Under §718.116 (condos) and §720.3085 (HOAs), the assessment runs with the unit, but we buy subject to it and price accordingly.

What about Cape Coral homes with seawall damage or canal-wall collapse?

Common after Ian. Seawall replacement runs $400–$600 per linear foot in Cape Coral, and the city requires permits through DEP and sometimes the U.S. Army Corps if you're on a Spreader Waterway. We buy the home with the seawall as-is and handle the rebuild.

Will you buy if I owe more than the house is worth after Ian?

Sometimes. If you're underwater because of post-Ian deferred repairs and a still-open claim, we can sometimes negotiate a short sale with your lender or structure a creative purchase. Send us the loan balance, the most recent statement, and any insurance settlement amount — we'll tell you in 24 hours whether the math works.

Do you buy mobile homes or manufactured homes in Cape Coral and Lehigh Acres?

Yes — both DMV-titled mobile homes (§320.015) and homes that have been title-retired to real property (§319.261) with the RP decal. Lehigh Acres has thousands of older single-wides and double-wides on owned land.

Ready to Sell Your Cape Coral House?

If your Cape Coral house has been on the market for six months and the showings dried up, if Citizens non-renewed you and the next quote is unaffordable, if the Ian claim is still in mediation and you just want out, if the snowbird trips don't make sense anymore, if you inherited a vacant lot from a grandparent and don't want to pay another year of taxes — call Byron at 951-331-3844 or fill out the form on this page. You'll get a written cash offer in 24 hours, a real Lee County title company on the contract, and a closing date you choose. No fees, no commissions, no repairs, no flights down from Toronto. Family-owned, 15+ years, 500+ Florida closings, BBB A+, 4.9★. We answer the phone.

Page current as of May 2026. Florida statutes cited (§627.7152, §627.351(6), §117.201, §193.155(8), §689.261, §718.116, §720.3085, §320.015, §319.261, Ch. 373 Part IV, F.A.C. 62-330) verified against flsenate.gov. Not legal advice — consult a Florida attorney for case-specific questions.